Quick Idea: Nexus Infrastructure $NEXS.L

This is the first time I’ve written something up in almost a year, so bare with me.

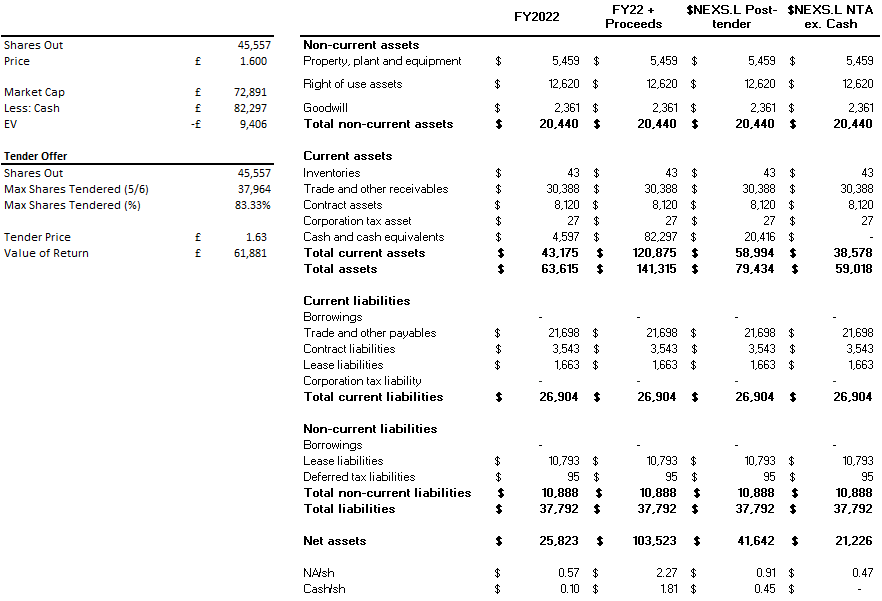

The $NEXS.L idea is fairly simple. The stock trades at £1.60 and has a market cap of £73M. On the 28/2 Nexus Infra announced - post completion of the divestment of two of its businesses, TriConnect and eSmart Networks for £77.7M - a planned tender offer to return £63M of the proceeds to shareholders at a price of £1.63/sh, with the balance being retained by the business.

This has given rise to an interesting situation because it appears to materially undervalue both $NEXS.L and by extension, the remaining stub. The first thing to consider is that $NEXS.L trades at a negative enterprise value. Compared to its market cap of ~£73M, there is roughly £82M in net cash, or £1.81/sh on the balance sheet post completion, therefore implicitly valuing Tamdown at less than £0.

Which begs the question - what might it be worth? Conceivably not £0, given it will have roughly £20M in cash and a similar sum in working capital, so what might be “fair” value?

Tamdown

Note that this is a fairly quick and crude valuation largely based on some hastily defined comps. I only wanted to get a sense of what Tamdown might reasonably be worth.

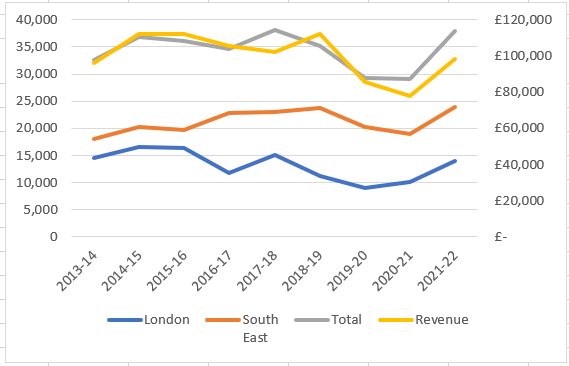

Tamdown is a UK based engineering contractor that performs “earthworks, remedial work, highways, substructures, basements and drainage systems”. Operations are concentrated in the South East of England and London and its customer base consists primarily of UK housebuilders. As can be expected for a contractor, margins are wafer thin even in a good year and levered to some sort of building cycle, which in Tamdown’s case is housing. You’ll note the tight visual correlation between revenue and housing starts in the chart below.

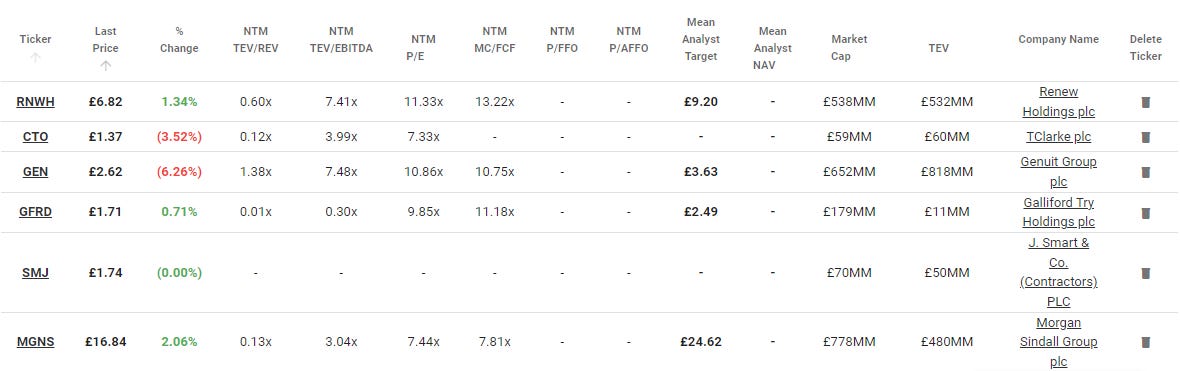

In terms of relative comps, I grabbed a list of quasi-UK building services contractors to form a basic peer group (no perfect proxies for $NEXS.L though), with a median PE ratio of 9.85x, or roughly 4-5x on a normalised, mid-cycle basis, which is what I’ll use to value Tamdown.

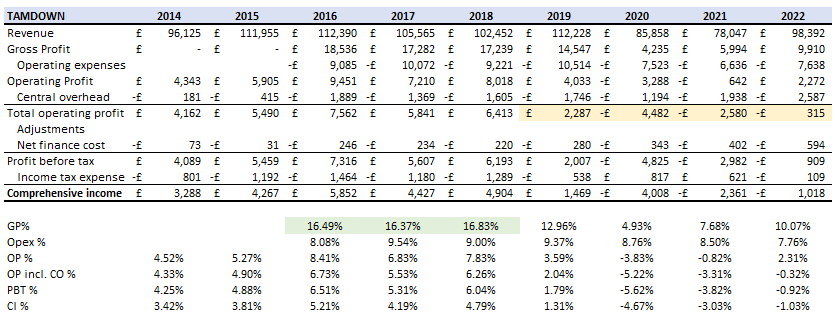

Setting aside the leaps of faith I’m about to make here, if we assume a return to normalcy - i.e without any further significant exogenous shocks like COVID-19, there is conceivably a path back to the historical gross profit margins of ~16% that Tamsdown achieved in 2016-18 prior to these events.

This will come via a combination of a) the operating leverage inherent to this type of business - optically you can see how each percentage point of gross profit in excess of ~10-11% falls to the bottom line once fixed costs are covered (contractors typically run tight ships), b) sequential margin improvement as historical contracts struck during COVID-19 run off and c) a return to more bountiful “macro” operating conditions, with pre-COVID levels of housing starts (but I’m not expecting this in the short term). It should also be noted that I’ve fully expensed central overheads to Tamdown, but this should fall by ~£900K to reflect the smaller size of the continuing group - so Tamdown pro-forma is probably £500K in the green at the operating profit level. Hence, YoY comps are all trending in the right direction.

With these assumption in mind, I believe Tamdown is probably worth anywhere from £15-20M, and the combined $NEXS.L entity around £31M if you take into account the net cash remaining after the tender offer. With the maximum number of shares tendered, the implied value per share is ~£4.08/sh. Whilst I’m not necessarily expecting it to trade this high given the prevailing economic conditions, trading up to at least net cash (£1.98/sh) still equates to a ~23% return.

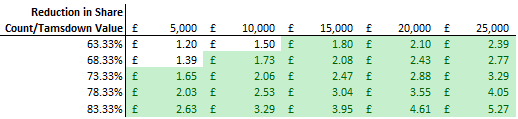

So how am I playing it? Importantly, I haven’t tendered any of my shares, as I see two potentially interesting outcomes from not doing so. Either a) shareholders recognise the value differential and force management to raise their price by voting down the tender offer (we will find out if this is the case shortly), or b) it goes through and I benefit from a highly accretive reduction in the share count, which is reflected in the sensitivity below:

Furthermore, management have indicated that they will only tender their Basic Entitlement, and will therefore retain at least a ~23% ownership in the stub. Logic would imply that if I’m saying the transaction is potentially highly accretive for me, then it similarly should be accretive for management if shareholders tender in excess of their entitlement - which I assume is an expectation that management has as they nurture retail towards a form of capitulation.*

Hence, even though I’ve acknowledged that management have stiffed shareholders with the price offered, I’m willingly hitching a ride anyway in the hopes that my smallish position will end up with a decent return through ownership of a larger piece of the economic pie. Fingers crossed & DYOR… it is the AIM after all.

*From my understanding of how this works in practice, for every one shareholder that does not tender their basic entitlement (5 shares for every 6 held), five shareholders will be able to tender in excess of their entitlement (5 shares for every 6 held, plus 1 for a total of 6). Post offer - in this hypothetical six person large register - the non-tendering shareholder will own 100% of the capital vs. ~16% previously.

Risks:

I spent roughly 2 hours on this.

Lots. This is an AIM shitco after all so I’m probably just another sucker about to get burnt.

Stewardship clearly isn’t great/management probably has an agenda.